Tips To Assist You Out With Your Home Mortgage

Created by-Sherrill McCoyYou can't just rush into getting a mortgage. Going forward without having enough information can have negative results. While you are getting your loan, if you have questions about the process, keep reading this article.

Start saving all of your paperwork that may be required by the lender. These documents include pay stubs, bank statements, W-2 forms and your income tax returns. Keep these documents together and ready to send at all times. If link web page don't have your paperwork in order, your mortgage may be delayed.

Get your documents ready before you go to a mortgage lender. You should have an idea of the documents they will require, and if you don't, you can ask ahead of time. Most mortgage lenders will want the same documents, so keep them together in a file folder or a neat stack.

If you are considering quitting your job or accepting employment with a different company, delay the change until after the mortgage process has closed. Your mortgage loan has been approved based on the information originally submitted in your application. Any alteration can force a delay in closing or may even force your lender to overturn the decision to approve your loan.

Be prepared before obtaining your mortgage. Every lender will request certain documents when applying for a mortgage. Do not wait until they ask for it. Have the documents ready when you enter their office. You should have your last two pay stubs, bank statements, income-tax returns, and W-2s. Save all of these documents and any others that the lender needs in an electronic format, so that you are able to easily resend them if they get lost.

You may be able to add your homeowners insurance costs to your mortgage payment. One advantage of this is negating the need to make two payments. Instead of paying your mortgage and an insurance bill, you can pay both bills in one payment. If you like to consolidate your bills, this is a good idea.

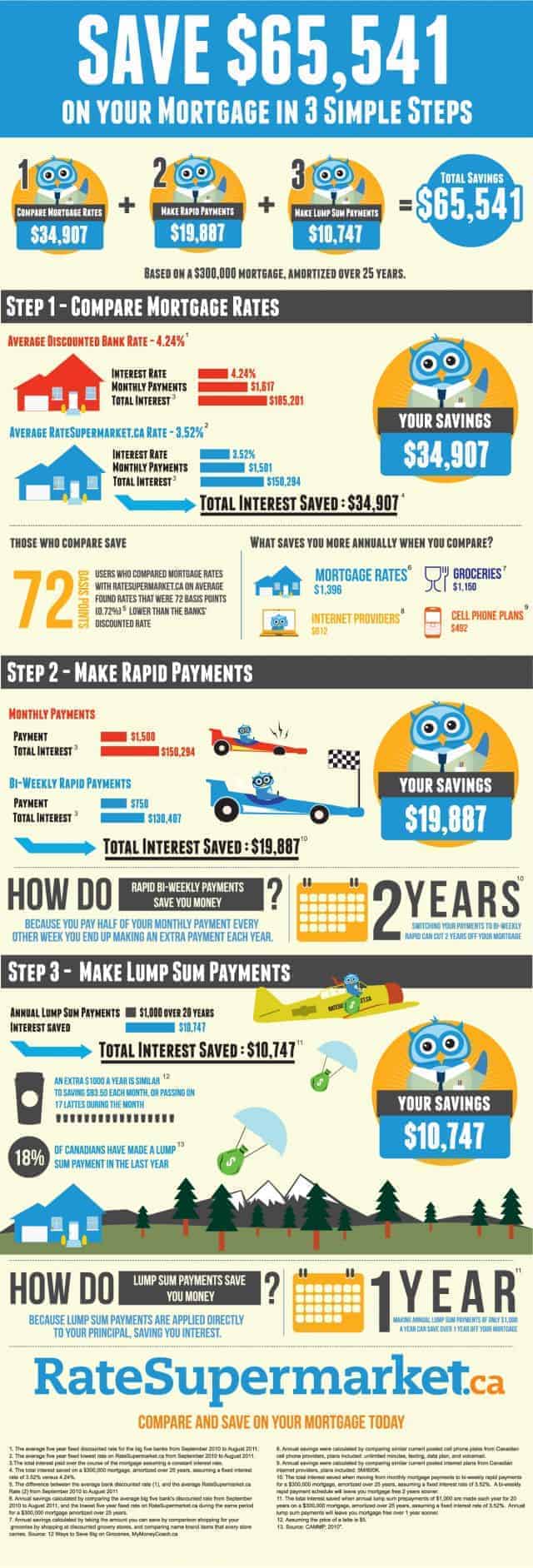

When financing a house, giving a large down payment will result in a lower mortgage rate. This is due to the fact that a big down payment will reduce your loan to value ratio. When the loan to value ratio gets lower, the interest rates become more favorable for the home buyer.

Get quotes from many refinancing sources, before signing on the dotted line for a new mortgage. While rates are generally consistent, lenders are often open to negotiations, and you can get a better deal by going with one over another. Shop around and tell each of them what your best offer is, as one may top them all to get your business.

Make sure you've got all of your paperwork in order before visiting your mortgage lender's office for your appointment. While logic would indicate that all you really need is proof of identification and income, they actually want to see everything pertaining to your finances going back for some time. Each lender is different, so ask in advance and be well prepared.

There are many different types of home mortgage loans available, and some are much easier to get than others. If you are having a problem getting a conventional loan, try applying for an adjustable rate mortgage or a balloon. These are short term loans ranging from one to 10 years, and need to be converted when they expire.

Current interest rates on home mortgages are lower than they have been in years. Experts expect them to begin increasing again shortly, so now is a great time to purchase a home and finance it at a low rate. The shorter the term of the mortgage, the better the rate you will be able to get.

Whenever you go to apply for a mortgage it is best to have a good overall financial situation. You have to have some money set aside for closing costs, your down payment, and things like inspections, credit report fees, and everything else you're going to have to pay for. If you have a large down payment, you will have a better mortgage.

Learn about the three main types of home mortgage options. The three choices are a balloon mortgage, a fixed-rate mortgage, and an adjustable-rate mortgage (ARM). Each of these types of mortgages has different terms and you want to know this information before you make a decision about what is right for you.

Pay at least 20% as a down payment to your home. This will keep you from having to pay PMI (provate mortgage insurance) to your lender. If you pay less than 20%, you very well may be stuck with this additional payment along with your mortgage. It can add hundreds of dollars to your monthly bill.

To obtain a home mortgage that's good, an excellent credit rating is necessary. Make sure you know your credit background. Examine your credit report for any errors and correct them to help improve your score. Consolidate your debts so you can pay less interest and more towards your principle.

Rebuild or repair your credit before shopping for a home mortgage. A good credit history and credit score qualifies you for a better interest rate. It is also frustrating to find the perfect house but not qualify for the loan you need. Taking the time to fix your credit before buying a house will save you money in the long run.

Understand what happens if you stop paying your home mortgage. It's important to get what the ramifications are so that you really know the seriousness of such a big loan as a home mortgage. Not paying can lead to a lower credit score and potentially losing your home! It's a big deal.

Get your credit under control. If you currently have a wallet full of plastic for every occasion, you should downsize. Having too much available credit can harm your loan, even if it is not debt. Close any non-essential accounts. Chose a gas card, a store card, and a single credit card to keep.

A home mortgage is usually the best way to finance a home. related webpage have to have a bit of education before you start the process of applying, though. Keeping the info you just learned in mind will help you own the home of your dreams.